In real estate investing, so much comes down to one thing: the appraisal.

As an investor, you’ll only close on a small percentage of the deals you actually analyze, underwrite, and submit offers on. And across all of those deals, value—whether that’s current as-is value or after-repair value (ARV)—is the most important metric in your underwriting. That’s why understanding the appraisal, and how it impacts your project, is critical.

At its core, an appraisal is a third-party opinion of a property’s market value, completed by a licensed professional. That value is used by lenders to determine how much they’re willing to lend on a specific transaction. Sometimes the appraisal comes in higher than expected, sometimes lower, and often right at the contract price or refinance estimate.

For investors, that number matters—a lot.

You’ve likely built your deal around an expected value. When the appraisal comes in materially lower than anticipated, it can disrupt your financing, your cash flow, and even the viability of the entire project.

A BRRRR Example: When the Numbers Shift

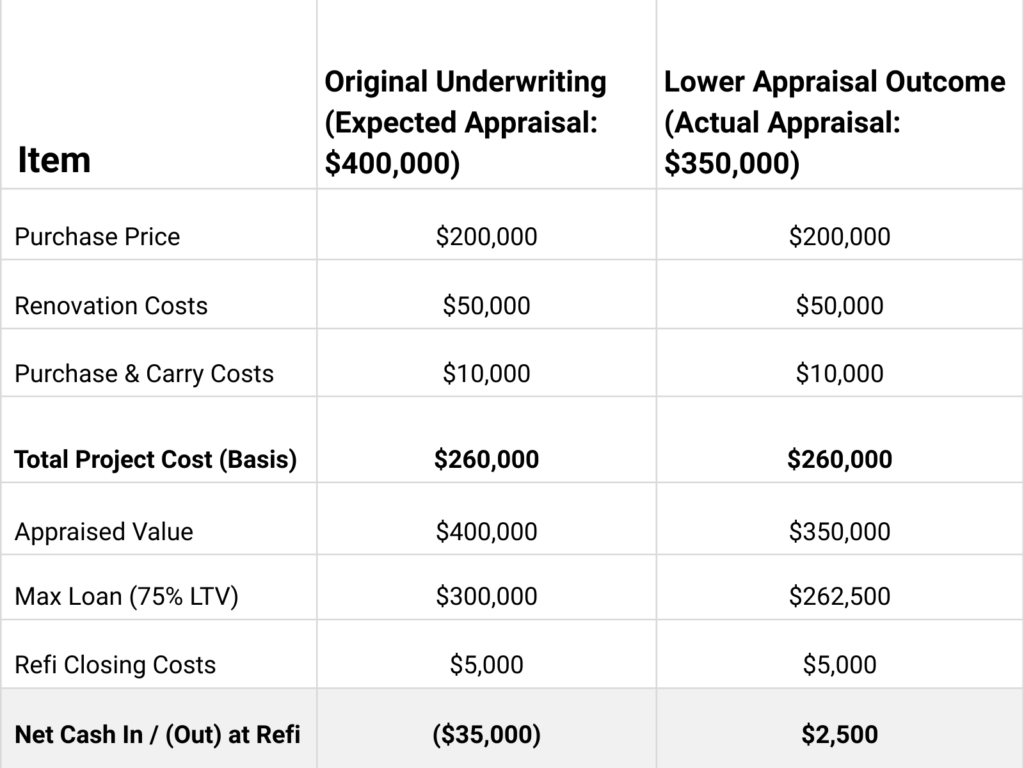

Let’s say you’re executing a BRRRR strategy. You purchase a property for $200,000, invest $50,000 in renovations, and incur roughly $10,000 in acquisition and carrying costs. All in, you’re into the deal for $260,000.

Based on your analysis, you expect an ARV of $400,000. With a 75% loan-to-value (LTV) cash-out refinance—typical for many DSCR lenders—you anticipate a new loan of $300,000. After paying off your total project costs and refinance closing costs, you expect to walk away from the refinance with roughly $35,000 in cash.

But what if the appraisal comes in at $350,000 instead of $400,000?

Now, 75% LTV supports a loan of only $262,500. After accounting for your total project costs and refinance expenses, you’re no longer pulling cash out—you’re bringing money to the closing table. Instead of receiving a check, you may need to bring roughly $2,500 to close the refinance.

Appraisal Impact on a BRRRR Refinance

Assumptions: 75% LTV cash-out refinance (DSCR loan)

A 12.5% drop in appraised value flipped a $35,000 cash-out into a $2,500 cash-in.

Same project. Same renovations. Same execution.

One different appraisal value—dramatically different outcome.

What to Do If You Disagree With an Appraisal

Appraisers are licensed professionals, and most do solid work. But like any profession, mistakes happen. Data can be incomplete. Comps can be imperfect. Judgment calls can miss important context.

If you disagree with an appraisal, here are practical steps investors can take:

- Provide your own comparable sales. Some appraisers won’t adjust their opinion, but others will. In many cases, appraisers simply didn’t uncover a key comp that materially impacts value.

- Share a detailed scope of work. If renovations were completed, provide line items, photos, and descriptions. The clearer the improvements, the easier it is for an appraiser to justify a higher value.

- Be present for the appraisal, if allowed. Meeting the appraiser at the property gives you the opportunity to explain renovations, rental income, utility responsibilities, and other relevant details.

Two Real-World Appraisal Issues

Over the past year alone, I’ve seen appraisal errors materially affect deals.

In one case, an off-market land deal came with a seller-provided appraisal that used a comparable sale from 2003. That outdated comp rendered the valuation unreliable and ultimately killed the deal.

In another case, an appraisal on a property we owned came in at $371,000 using poorly matched comps. After disputing the report and submitting more appropriate comparables, the appraiser revised the value to $452,000.

The takeaway? Appraisals aren’t infallible. They’re opinions—backed by data—but still opinions.

Appraisal issues will happen. When they do, your job as an investor is to provide clear, credible evidence to support fair market value and protect the integrity of your deal.

Thanks for reading this week’s Experience, and best of luck on your real estate investing journey!