One of the most common questions in real estate investing is simple—but critical: Is this a good deal, and what should I pay for it? That question becomes even more important when a property is being sold at auction, where there’s no predetermined purchase price. In every situation, the numbers have to guide your decision.

Let’s walk through a real-world style example and show how DSCR underwriting can help you establish a clear, defensible purchase price.

The Deal Setup

A property has just hit the market in our local area and will be sold at auction.

The property that will be sold at auction.

The auction’s terms are fairly standard: the seller will provide clear title and transfer taxes are split between buyer and seller. For this example, we’ll assume the property is rent-ready—no renovations required.

Based on comparable rentals in the area, market rent for a property like this falls between $1,600 and $1,800 per month. We’ll use the midpoint, $1,700, as our working assumption.

The plan? Buy and hold as a long-term rental using a DSCR loan.

So the big question becomes: How much can you pay and still make this deal work?

Understanding DSCR (Debt Service Coverage Ratio)

DSCR loans are underwritten primarily on the property’s cash flow rather than the borrower’s personal income. While guidelines vary by lender, many look for a DSCR of 1.20 or higher to offer the most favorable terms—especially when paired with an 80% loan-to-value (LTV).

DSCR is calculated as:

Rental Income ÷ (Principal + Interest + Taxes + Insurance + HOA/Condo Fees)

- DSCR = 1.0 → The property breaks even

- DSCR > 1.0 → Positive cash flow

- DSCR < 1.0 → Negative cash flow

In short, the higher the DSCR, the more comfortably the property covers its debt obligations.

Running the Numbers

To analyze this deal, start by inputting all known variables:

- Monthly rent: $1,700

- Property taxes: Known amount from public records

- Insurance: Estimated conservatively (or quoted ahead of time)

- Interest rate: Assumed at 6.5% for this example

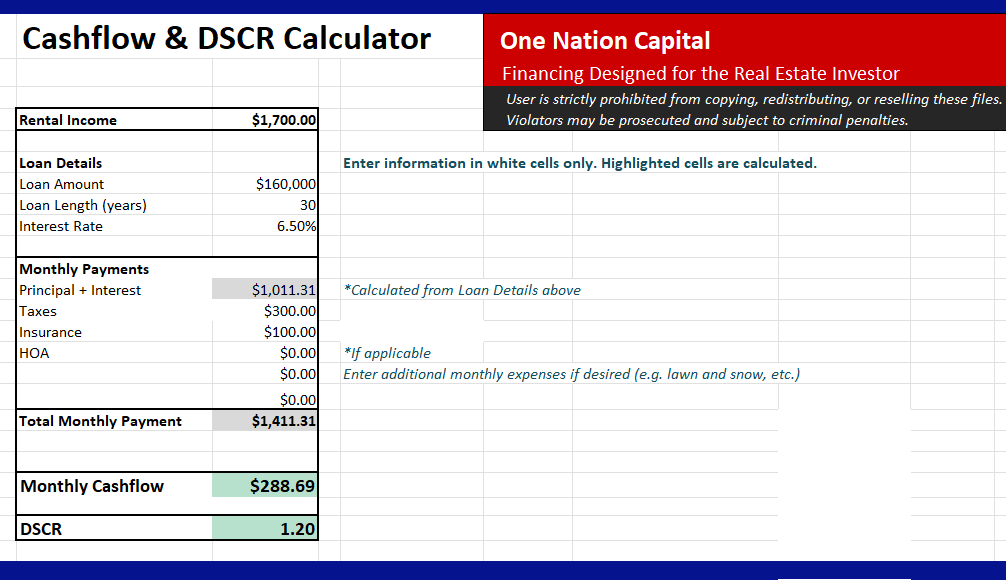

Making the math easy: the numbers from the deal entered into a Cashflow & DSCR Calculator, which you can check out here.

From there, you can adjust the loan amount until you hit a target DSCR of 1.20.

After running the calculations, the numbers show that a loan amount of $160,000 results in a 1.20 DSCR. At an 80% LTV, that translates to a purchase price of $200,000.

This gives you a realistic ceiling for your auction bid—one that aligns with lender guidelines and your cash flow goals.

What Does the Cash Flow Look Like?

At this price and loan structure, the property would hypothetically generate approximately $288 per month in positive cash flow after covering principal, interest, taxes, and insurance.

That’s not just a guess—it’s the result of underwriting the deal before making an offer. Whether you use a spreadsheet, a calculator, or a dedicated real estate analysis tool, the process is what matters most.

By laying out the numbers visually, you’re able to see how rent, loan amount, and expenses interact, and this makes it easier to understand how small changes impact the overall deal.

A Quick Note on Auction Properties

An important caveat: clear title matters. DSCR lenders will not fund properties with unresolved title issues.

Something else to consider is the required timeline to complete the purchase. Most DSCR lenders will take between 4-5 weeks between loan application and settlement. If the auction requires a 30 day settlement, you may be short on time.

Always factor this into your auction strategy and due diligence.

Final Takeaway

DSCR underwriting doesn’t have to be complicated. By starting with realistic rent assumptions, understanding lender guidelines, and working backward to your purchase price, you can approach auctions—and any deal—with clarity and confidence.

When the numbers work, the deal makes sense. When they don’t, it’s better to walk away than to force a purchase.

Thanks for reading, and best of luck on your real estate investing journey!

-BROCK